We’ve all had emergencies. From car wrecks to sudden job layoff. And when an emergency hits, it can feel as if everything in your life is going wrong.

Emergencies are stressful – and struggling to pay for them enhances the problem. By setting up an emergency fund today, you can ensure that you're ready when the next emergency strikes.

What is an emergency fund?

An emergency fund is money you save to pay for an emergency. Emergency funds should be kept in a separate account from your everyday spending to ensure that they aren't accidentally spent.

Having an emergency fund in place can save you from wracking up credit card debt or missing out on bill payments when an emergency strikes.

What defines an emergency?

That’s really up to you and your family. The dictionary definition talks about unexpected events that need immediate attention. This can be anything from medical problems to property damage or a job loss. It’s true that emergencies are almost always unexpected, so it’s good to have a plan before.

When you start an emergency fund, talk with whoever you share a budget with about what defines an emergency. Make a list of things you agree ARE emergencies, as well as what is NOT an emergency. Create an accountability system to be sure you’re using your emergency funds on emergencies only.

How much should I save for an emergency fund?

Most people say a good amount to have in your emergency fund is 3-6 months of expenses. If you get laid off of work or are injured and unable to work, this would help you get by. Of course, it takes time – several months, even years – to get to this point. You can start out with a smaller emergency fund of $500 or $1000 to cover small emergencies.

When determining your monthly expenses, take a look at your budget. Your monthly expenses are everything you pay for each month. Your rent, electric bill, car payment, health insurance, and other fixed bills should definitely be included. Then, you’ll want to figure out how much you spend on things like food and gas, which may not be a fixed expense but are things you’d still need to pay for.

Your emergency fund should have enough to pay for everything you need each month. Bills don’t go away if you suddenly lose your income. Having an emergency fund helps while you look for another job or heal from an injury. Listing all of your expenses can help you know how much you need in your emergency fund.

If you have a life change coming soon, like a baby or retirement, bulking up your emergency fund is a good idea. Life changes can bring new or different expenses, especially if it involves time off work (like having a baby). If your job has regular layoffs, it’s also good to have a full emergency fund as soon as you can.

How do I start saving for an emergency fund?

A common reaction to the idea of an emergency fund is “I don’t have any money to save.” If you are already in over your head because of a past emergency, it’s even harder.

I get that. I really do. However, if you don’t think you have money now, will you have money when there’s an emergency? I promise it’s easier to find a little money to start saving now than a huge amount when there’s an emergency to pay for.

Take a look at your budget and look for places you could find money to put in an emergency fund. Even if it’s just a small amount, you’re still doing your future self a favor.

Even if you have to start out small, with just $20 every paycheck, it’s worth it. If you get paid twice a month, you’d have almost $500 after a year of sticking $20 back per check. Ideally, you’d be able to do this without having any emergencies to dip into it for. If so, you have a nice start to an emergency fund.

Consider getting a small side job, or selling extra things around your house you don’t need anymore. Having a yard sale can help you declutter and also help you start your emergency fund. There are also free money-making apps that can help you make a little extra money. Pick a way to make some extra cash and put what you earn right in your emergency fund.

If you get a sum of money, like a tax refund or an inheritance, use some for an emergency fund. Tax refunds are kind of like a savings account anyway, because it’s really your money. You didn’t bring it home during the year, but instead get it paid out once a year. Using some of this money for an emergency fund is a way to be wise with this “savings account”.

Finding money to start an emergency fund may take some creativity. Whether you have a garage sale or get a side hustle, there are lots of ways to get extra money to save. Your future self will thank you!

Where should I keep my emergency fund?

You’ll want a separate account for your emergency fund so you aren’t tempted to dip into it. The emergency fund should be easy to get to in an emergency, but not so accessible that you'll be tempted to spend the funds on everyday purchases.

You can open a regular savings account at any bank or credit union for your emergency fund. You can also use an online savings account like Simple Bank or the Qapital Savings app. Putting your money in a savings account isn’t going to earn much extra, but it is stable.

If you set up a checking account you can have a separate debit card to pay for emergencies. But having this easy access to money can be tempting. If you do get a debit card, be sure it’s clearly marked so you don’t accidentally use it instead of your regular card!

Another option is a money market account. This is like a savings account because it pays interest, but you’re able to write checks or have a debit card too. Money market accounts have some special rules and you often need a certain balance, but can make a good emergency fund.

If you feel you’re in a spot where you can be riskier with your emergency fund, you can invest it. It’s still a good idea to choose a conservative investment to lower your risk of losing money. Additionally, you’ll be able to earn some extra money when you invest your emergency fund.

Consider investing once you’ve put a decent sum of money into a traditional emergency fund account. If you have 3 months of expenses in a regular account, think about investing the other 3 months of expenses.

Using a robo advisor, like M1 Finance, can help you choose a conservative investment. M1 is free to use, but you do have to have at least $100 in your account. M1 is a great tool to help beginning investors learn the ins and outs of investing.

Sites like Betterment also help you plan how to invest and meet your goals. Betterment does have a small fee, but doesn’t have a minimum balance. Betterment’s website walks you through everything you need to know to get started.

Why do I need an emergency fund?

None of us are immune to emergencies. If it’s not one of the emergencies we’ve already talked about, there are countless more. Emergencies are a fact of life, and you should be financially prepared for them. The peace of mind of having an emergency fund helps you focus on the actual emergency, not how you’ll pay for it.

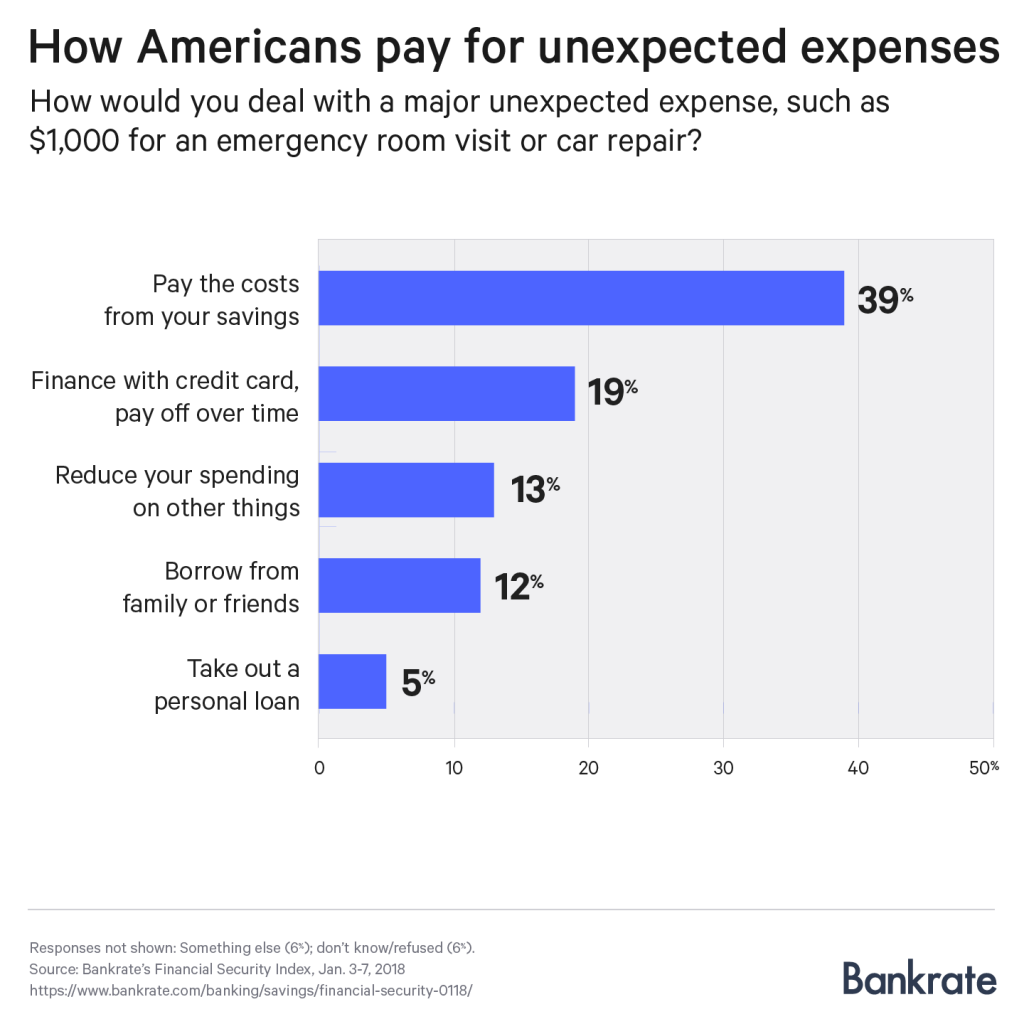

A Bankrate Financial Security Index survey came out in January 2018 and found only 39% of Americans have $1,000 in savings to pay for an emergency. That means over half of Americans don’t have a cushion for emergencies, and would likely have to go into debt to cover one.

Whether it’s borrowing from a relative, putting it on a credit card, or taking out a loan, adding debt adds stress. Added debt can create long term financial stress, in addition to the stresses of the emergency itself.

Conclusion

An emergency fund is a separate account where you save to pay for necessary, unexpected expenses. An emergency fund is considered fully funded when you have enough saved to cover 3-6 months of expenses. Even if you aren’t able to save this much right away, starting with $500 or $1000 can be a lifesaver.

Emergencies happen to everyone, and they’re often expensive and inconvenient. Saving now for future emergencies is a favor to your future self. By building out your emergency fund today, you'll be well prepared for whatever surprises arrive tomorrow.